You're reading for free via Dividends Forever's Friend Link. Become a member to access the best of Medium.

Member-only story

Here’s How You Build An Excellent Credit Score

Do you like free stuff?

Are you capable of paying your bills on time?

If so, you can earn hundreds (or even thousands) of dollars in free rewards every year — all by using credit cards responsibly.

This means 2–3% cash-back each month, multiple $200 sign-up bonuses every year, and other cool rewards like free hotel stays or gift certificates.

Doing this also builds up your credit score, giving you access to low-interest loans and reasonable mortgage rates. If you ever need to borrow money for a house, or want to lease a car, having good credit can save you tens of thousands of dollars.

Here’s how you can build an excellent credit score, starting from zero.

Zero To Excellent In Three Years Or Less

In January, 2020, I had no credit.

Like many people, I was under the impression that credit card users had to carry a balance. And that paying with credit cards forced you into debt.

This is false.

As long as you pay your card off on time, you aren’t penalized. There’s no interest payment, and anyone with basic budgeting skills can easily keep themselves out of debt.

Don’t go crazy buying things, and remember the payment due date.

That’s it.

As long as you have a card with no annual fees — there’s zero downside to this method.

Now, here’s the catch…

Building credit is a lot like playing a video game.

When you start playing a new game, your character is weak and doesn’t have the best weapons or items. And you have to play for a while before unlocking upgrades and better equipment.

Building credit is the same way.

If you’re starting from zero, you’re locked-out of some of the best cards (more on that in a moment) and there are a lot of scams or unfavorable offers being pitched to you.

In 2020 when I decided to start building credit, I was 26 years old with no credit history.

Starting out, I felt like I was too old to build good credit.

Or, that I should have learned about credit cards earlier.

You might be in the same situation.

In which case, I have good news for you. It’s not too late. And you can easily build yourself up to an excellent credit score within the next 2–3 years.

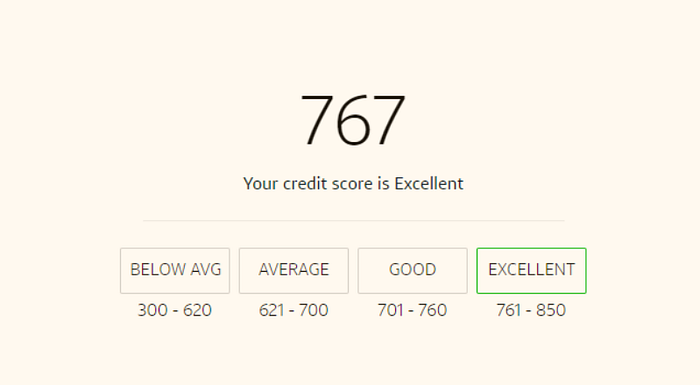

In fact, here’s my credit score right now.

I went from a 380 “bad credit” score, to a 767 excellent credit score in about three years. And I did it by applying for no-fee cards and paying my balance off on time.

If you want to improve your credit score, build a portfolio of 2–3 no-fee credit cards and pay your balance off.

It’s that simple.

Three Great Starter Cards

A lot of “starter cards” or “credit builder cards” are scams.

No-name banks will mail you offers for cards with zero rewards and hefty annual fees.

Don’t take these, they’re a rip-off!

Many legitimate financial institutions already have starter and credit builder cards. And these have no annual fees, while offering some benefits.

Here are three of the easiest, no-fee starter cards you can apply for.

1. Discover it Cash Back Secured Card

This is the first card I ever received, and it’s specifically designed for people with no or poor credit.

The Discover it Cash Back Secured Card is very simple.

You apply for this card and pay Discover a refundable security deposit.

Your security deposit then acts as your line of credit. So if you deposited the minimum amount of $200, you have a $200 line of credit every month.

After paying your balance off on time for 7 months, Discover will refund your deposit and turn your secured card into a regular credit card.

Typically, they’ll also bump-up your credit limit. And this has a huge benefit to your credit score.

The Discover it Cash Back Secured Card also rewards you with 2% cash-back at grocery stores and restaurants, 1% cash-back on all other purchases, and a special “Cashback Match” which doubles all the cash back rewards you’ve earned during your first year as a cardholder.

You also get an exclusive $50 statement credit if you sign-up using this referral link.

2. Capital One Platinum Secured Credit Card

Another card that’s easy to get.

The Capital One Platinum Secured Credit Card doesn’t have any welcome bonuses or benefits. But it is a no-fee card. And the security deposit is much lower than Discover’s.

With the Capital One Platinum Secured Credit Card, you pay a refundable security deposit (this one as low as $49) and are given a line of credit.

After 6 months, the Platinum Secured converts to a normal credit card.

And, you receive your deposit back as a statement credit.

The two nice things about this card are the low deposit requirements (when I applied, I put $49 down and got a $200 line of credit) and the fact that this card is accepted globally without any transaction fees.

If nothing else, this is a decent back-up card for anyone who travels abroad.

And, using the Capital One Platinum Secured Credit Card will boost your credit.

If you’re interested in this card, you can sign-up through this referral link.

3. American Express Blue Cash Everyday Card

While American Express is often associated with prestige credit cards and big-spenders, they also offer an easily accessible line of no-fee cards.

The American Express Blue Cash Everyday Card is a great starter card with a fantastic welcome bonus and plentiful cash-back opportunities.

Unlike the other two cards on this list, this one does require some credit history. But it’s not a massive hurdle. I actually applied for this card within my first year of credit-building, and was approved immediately.

The American Express Blue Cash Everyday Card rewards you with 3% back at U.S. supermarkets and gas stations, 3% back at online retailers, and 1% back on all other purchases. There’s also a $200 welcome bonus statement credit that’s automatically applied after you spend $2,000 within the first 6 months.

You can enjoy the $200 welcome bonus by signing-up through this referral link.

How To Use Your Cards

Once you have a starter card (or two), the best way to build credit is by underspending.

If you have $500 in monthly buying power, make a few small purchases.

But don’t go above 50% of your credit limit.

Maxing out cards or using too much credit can actually lower your score.

So if you have the Discover it Cash Back Secured Card, for example, use it to buy groceries or gas. This way you’re getting the 2% cash-back on something you already need.

Or, use your Capital One Platinum Secured Credit Card for little things like a cup of coffee or small Amazon purchase.

Again, like a video game, you’re starting small.

But after 6–7 months, you’ve built up your credit and upgraded your buying power.

Here’s What Happens When You Have Excellent Credit

Play the credit card game intelligently, and you get a lot of free stuff.

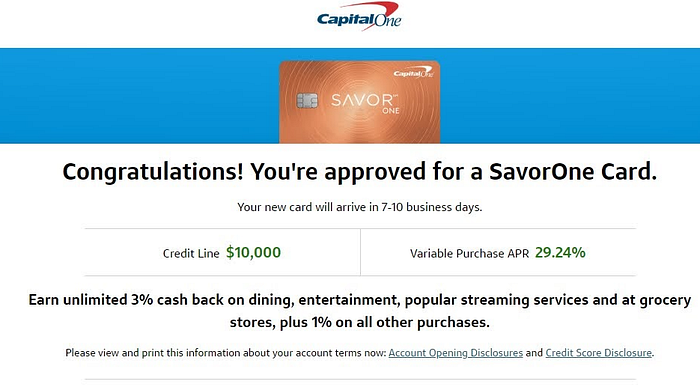

I want to buy a new phone this year.

The phone I’m looking at costs $300. Rather than pay that in cash, I leveraged my good credit score and applied for a new Capital One SavorOne card.

If you have fair to good credit, there’s no welcome bonus.

But if you have excellent credit, Capital One gives you $200 when you sign-up.

That $300 phone now costs $100.

Once you achieve excellent credit, banks and financial institutions pay you.

You also get preferable mortgage rates, can access high-reward credit cards for free airfare or hotel rooms, and receive exclusive discounts from major retailers.

Building excellent credit costs nothing. Yet the rewards are huge.

Disclaimer: This article is for entertainment purposes only. It is not financial advice, always do your own research. Also, this article contains referral links to help support Sad No Coiner.